TrueNorth Speaks at ABI – Loan-to-Own Northeast Conference

Introduction

As an investment banker (“IB”), I have been representing companies in the purchase and sale of distressed businesses in the middle market for more than twenty-five years. I need to ask the reader to (1) provide me a bit of latitude on use of legal terms and concepts (I am not an attorney), and (2) presume I am addressing predominantly, privately-owned businesses in the bottom half of the middle market (capital structures typically no more complex than equity, senior secured and junior capital).

Overview

I have come to believe that the term “sale” may be a misnomer in a distressed situation. As you read on, presume that I am referencing businesses that are overleveraged and/or require new capital in support of a turnaround plan. This rescue capital will require substantial targeted returns (equity returns) for the risk undertaken to right the business. What is really happening is less a “sale” and more a creation of value (where little or none existed for the equity). In a conventional sale process, one presumes the goal is highest and best value. Highest and best value does not ensure potential value creation, at least not for the prospective investor (new capital).

Value creation may be enhanced in “Loan to Own” transactions. Loan to Own transactions are characterized as the purchase of the secured debt position with the goal of either being paid at par or using par value to acquire the company. The debt is usually purchased at a discount and then credit bid in a 363 sale or foreclosed “peacefully” pursuant to Article 9. The discount dictates the extent to which value is created for the rescue capital, even before greater value may be realized through a turnaround plan.

There are risks involved with this strategy—liquidation risk, i.e., the company fails and liquidation value is less than what was paid for the debt; litigation risk, i.e., the debt purchaser becomes the target of subordination, re-characterization, breach of fiduciary duty, or fraudulent conveyance claims; and “value” risk, i.e., the risk that other investors believe that the company is worth more than the debt acquirer, although in this situation the debt acquirer’s downside is payment at par, the risk is that the debt acquirer ends up not owning.

So why use this strategy, what is the financial advantage for the investor, as it is usually the investor calling the shots? How does using the Loan to Own strategy create value that other strategies do not, and, enough that an investor would decide to use this strategy given the risks? The short answer is control.

The Distressed Sale Process vs. the Conventional Sale Process

I do believe that there is a methodology and calculus that should be employed when evaluating a strategy for a “sale” or purchase of (or attracting capital to/investing capital in) a distressed business, and in particular by a potential new owner/provider of rescue capital. Critical to understand the unique aspects of distressed sale vs. conventional sale and the varying interests of the parties.

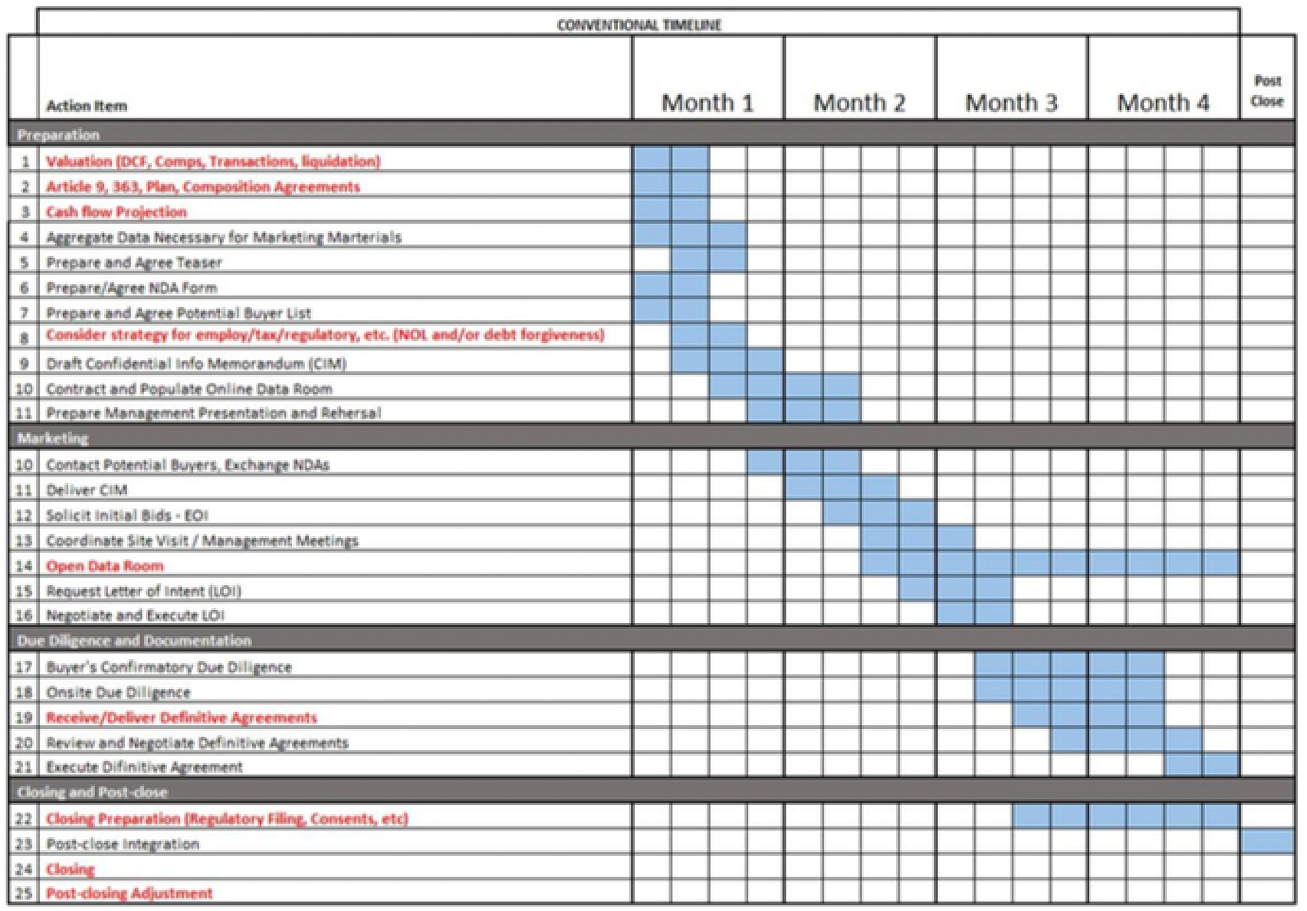

The above timeline (click to enlarge) summarizes typical steps in a sale process and highlights in red the steps that are different for a distressed vs. a conventional sale (for a conventional sale this process would likely be depicted as six to nine months):

In the simplest sense, for a going concern, value is represented by the present value of annual future free cash flow. For a distressed business, where positive cash flow, if any, discounts to less than the sum of liabilities, and the ability to operate absent capital infusion is in question, the liquidation value of the hard assets will drive value. Additionally, the time frame shortens from annual to monthly, and even weekly, projections. As IBs, we know that potential investors or buyers will seek to pay no more than a modest premium to liquidation value and many will discount further for anticipated future capital requirements to underwrite the turnaround plan.

In a conventional “sale” process, the seller is typically seeking their personal optimal intersection of: highest value, optimal structure, certainty of close, time to close and post close disposition of the business and the employees. Most importantly, in a conventional sale of a healthy business, the seller has the luxury of time to seek their optimal outcome. In a distressed “sale” process, the seller is typically seeking optimal structure, certainty of close, time to close, reduction of personal exposure and post close disposition of the business and the employees. The seller does not have the luxury of time, and, most importantly, highest value takes on a very different meaning (and is explained further below).

The current equity interests’ protection is to try to control the sale/investor process for as long as possible. It is atypical to request a non-circumvent provision in a non-disclosure agreement in a conventional sale process and paramount to request one in a distressed process. Sophisticated investors will attempt to negotiate directly with secured creditors. The equity interests’ ability to inject itself between creditor and investor often represents their only leverage.

Investors (rescue capital) will weigh optimal financial outcome, transactional control and perceived (litigation) risks in determining whether they proceed with an investment and then, how they may structure such investment.

The creditors will weigh these offers against liquidation value, less legal and collection costs, time, and the cost of internal resource (devotion of manpower to a slow process). Because the equity owner is out of the money, despite fiduciary duties and possible personal exposure, the interest of the equity often becomes adversarial to those of the creditors. Private owners, particularly those with personal guarantees, will become natural competing bidders if they cannot align their interest with that of the investor.

Other differences between a conventional and distressed process include:

(1) Cash flow – in a distressed sale the ability to identify how the business will fund operations through a closing is top of the list for obvious reasons. Call this step one;

(2) Tax Implications – consideration of tax implications for debt forgiveness is not an issue in a conventional sale but can have dramatic implications in a distressed process and can force a legal mechanism if NOLs are not available as a shelter;

(3) Timing – because there is no luxury of time (time is of the essence), there is typically a more relaxed approach to confidentiality concerns. I am not suggesting protections, such as non-disclosure agreements (“NDA”), are any less important. However, the latitude to negotiate NDAs, the early opening of data rooms, and the earlier disclosure of more data, all in the interest of moving quickly, tends to be the norm;

(4) Purchase and sale (“P&S”) agreements – both buyer/investor and seller need to recognize that P&S agreements will be abbreviated. Specifically, representations and warranties are less significant as there is often no solvent individual or entity to stand behind them. Representation and warranty insurance is usually cost prohibitive in these situations;

Finally, in the middle market, and particularly with privately-owned businesses that are in financial distress, business viability and capital requirements to achieve business viability are of critical importance. A credible pro forma is what is being “sold” by the IB. “Credible” cannot be over-emphasized. The IB that understands the distressed market knows that there are investors that focus specifically on “special situations”. The IB gets a few minutes on the phone to capture the investors interest. The plan had better be simple and, ideally, it will not hinge on revenue growth (deemed the riskiest proposition by investors) only.

Given the above, when should the investor choose/consider the loan to own strategy? In the distressed sale, where the business is over leveraged and underperforming, a legal mechanism should be employed to reduce the leverage (and create value): sale of assets pursuant section 363 of the Bankruptcy Code, friendly foreclosure of assets pursuant to Article 9, composition agreements outside of a formal bankruptcy proceeding, receivership, assignment for the benefit of creditors or a plan of reorganization pursuant to a bankruptcy filing.

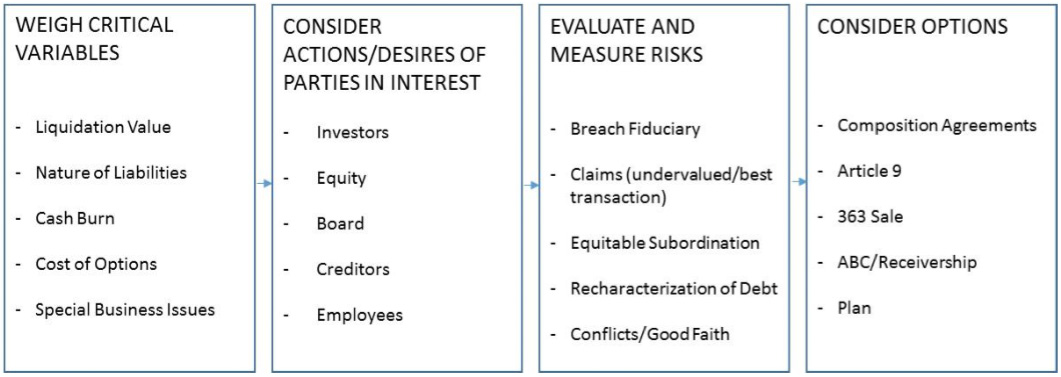

Assimilation of Data and Analysis of Optimal Path

Loan to Own and a 363 sale or Article 9 friendly foreclosure are not mutually exclusive. Owning the debt can improve an investors position regardless of legal strategy employed to deleverage. There is not an absolute clear optimal path at the outset. There are likely best paths, however, the fluidity of the situation dictates a possible need to pivot for changing circumstance at any moment. Some of the obvious variables that will influence direction include: (1) Business performance during the process, (2) Outside influences on the Business i.e. customer, supplies key employees etc., (3) changes in the market and economic climate during the process, and, perhaps most importantly, (4) the rescue capital’s appetite for risk (nature of the winner).

Specific advantages of Loan to Own include speed and control. The purchase of debt of target may reduce time to transaction by months due to ability to force the process. Owning the debt may provide an ability to limit or cut off equity’s control/leverage mentioned above. An investor can enhance its ability to dictate (to a degree) terms to other creditors, vs. taking terms as negotiated by others if a stalking horse. Control is further realized through an ability to limit competition. Particularly where an investor provides working capital and other financial accommodations, will a competing buyer want to step in?

Despite possible advantages for the investor, Loan to Own is not a default position. If composition agreements can achieve the desired result, this path may be favored as it is likely more favorable to the business owner, the least costly path, minimizes litigation risk and maximizes transactional control. However, with composition agreements, it can be difficult to achieve the optimal financial outcome due to creditor holdouts. You cannot compel a creditor to take a discount or long-term payment plan without employing one of the other legal mechanisms mentioned above. Article 9 will most often be the second choice (363 third) for “sophisticated” investors (transactional control with same financial outcome with lower transaction costs if risks can be quantified and are deemed manageable).

DISTRESSED CALCULUS FOR OPTIMAL PATH

The diagram above (“Distressed Calculus for Optimal Path”) lists outcomes in preferred order for the investor based upon transactional and cost control, assuming reasonably similar financial outcomes can be realized. Investors are not really identifying the best option so much as eliminating options that do not achieve the desired capital structure with legal and operating risk acceptable to them. In other words, why go to the time, expense and possible risk of a 363 sale if composition agreements or an Article 9 friendly foreclosure can deliver the investor a reasonably similar outcome (without transactional control risk – overbid risk)? And, of course, if any option provides limited chance to create value, why make any investment?

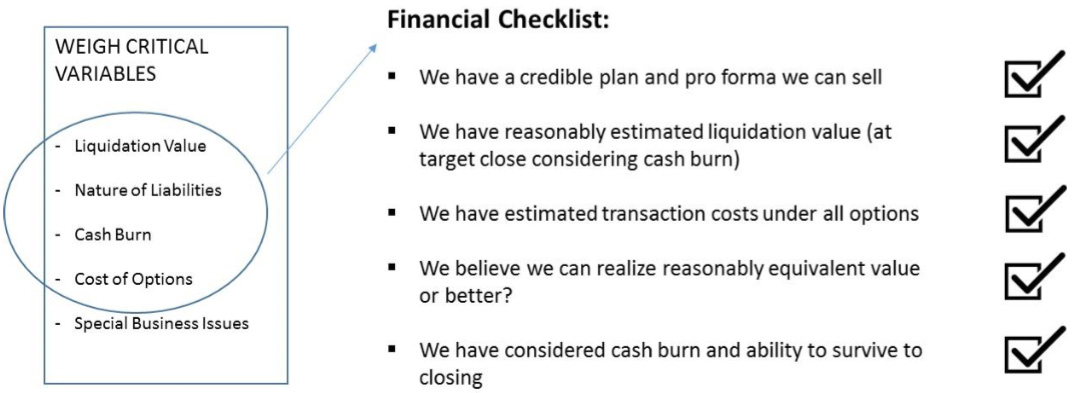

The below “Financial Checklist” reflects the initial steps in evaluation of “Optimal Path”. The steps are employed to evaluate the overriding question: will any party in interest, in the money, be disadvantaged by the restructure and have a legitimate claim?

When the IB has completed his review of financial considerations, the question of “Special Business Issues” and legal risk remains. This will highlight the need for a team comprised of IB and attorney to plan from the outset. There are any number of issues that might preclude use of one or more of the legal mechanisms to deleverage. Examples would include regulated industries such as banking, shipping, government contractors and utilities where formal proceedings can have implications for day to day operations. Furthermore, special circumstances such as multi-employer collective bargaining agreements (withdrawal liabilities) or significant environmental or other successor liabilities (warranty or product liability for example) can impact decision making.

Finally, the questions remains’ whether will legal risk/cost will be a show stopper? This depends on the buyer’s appetite for risk/reward? It can be very difficult to quantify risk and cost given the relatively unsettled areas of law and varying positions of judge. If an investor goes the Loan to Own route, they have to go in estimating litigation cost and their appetite for risk.

It bears repeating that he evaluation process requires careful coordination and collaboration of the company’s counsel and IB. Identifying optimal path is an iterative process and not the same for all parties. In summary, the IB considers/addresses value, likely nature of interest and optimal structure. Counsel outlines the risks associated with a path. IB works with counsel to quantify the risks. Path is adjusted based upon the investor appetite for risk (as weighed against cost, control and timing). Change a variable, reconsider the path.